Millennials Part II – Affordability isn’t the argument!

Millennials – Part II – Affordability isn’t the argument!

Wow, what a response to part I of this Blog. We have had so many comments on our website and the comment threads on our Facebook page were literally hundreds long. The overall response was that you agreed with my sentiments.

But, of course I had so many comments complaining and saying I know nothing and that I am part of the problem. I even had two guys wanting to punch my face in. Yeah, whatever… Now for those Millennials who have purchased a home or investing like crazy – awesome and congrats!

If you missed it, here is the Blog link and link to the Facebook page so you can see the comments. Have a scroll down and enjoy the comments!

So in this Blog, I wanted to address some of the comments. The issue being that many of the comments were ill informed and obviously influenced by media and the crap they publish. Then in part III of this Blog, I am going to offer several solutions to this problem. So, let’s start:

Firstly, I want to make it absolutely clear – at no stage did I ever say buying a home was easy. Not when my parents purchased their first home, not when I purchased my first home and not now. If it were so easy then everybody would own a home and there would be no investment properties, nor tenants.

Is it achievable though? – Absolutely.

As a Buyers Agent and Mortgage Broker, I see and write many loans for Millennials who are doing exactly this. Some, with no help from their parents either.

A common theme to the comments were that youth employees earn less. Well, yes they do, but this Blog is about Millennials. And Millennials are born from 1980 to 2000. Making them up to 36 years old. Now youth is for people up to 24 years old. I would have thought a Millennial would have know they were a Millennial, but that obviously was not the case. Just wanted to clear that up!

I had a lot of people commenting that the median Sydney and Melbourne property prices are 10 to 12 times annual incomes. And in Sydney the median household income is $140,000 gross which is approximately $94,000 net. The Sydney median house price is $995k. This equates to around 10 times annual income.

SO WHAT!!!

As a first home buyer, you buy at entry level. Just like I did, all my friends did and just like my parents did.

I copped some flack that I was earning an income of $18,000 and bought my first property for $112,000, being that it was less than 6 times my annual income. Now, had they read the Blog correctly, my income of $18,000 was for 6 full days work. My normal salary, working it out in my head, would have been approx $13,500.

Now on those figures, the real figures, it’s was 10 times my salary. Purchased when unemployment was 10.5% not 5%, youth unemployment was 39% not 13.5%. The loan term was over 25 years not like today at 30 years and interest rates were 11.75% not 3.88%.

As you can see, buying in “the recession we had to have” was not all roses either. But we did it!

But where all your comments have gone wrong are comparing your salaries to the median salary and the median house price. What moron drummed this measurement into your head? Sure it’s a measurement for economists to banter on about, but unless you sell a tech start up, inherit a ton of cash or win Keno, you ain’t buying a million dollar house as your first home.

And just a little wake up call, 99.9% of ALL of us didn’t either.

So why not, do your numbers on entry level properties, which is what you’ll be buying. Oh I know it’ll be a one bedroom unit in a suburb not in the CBD or on the beach, but it’s a home… And isn’t that your argument?

The biggest underlying message I received from the Millennials were that they were not willing to adjust their expectations for their first home. They are expecting to buy a three-bedroom home in the 5klm city CBD radius.

Reality check – most people cannot afford a house within 5klm of a major CBD.

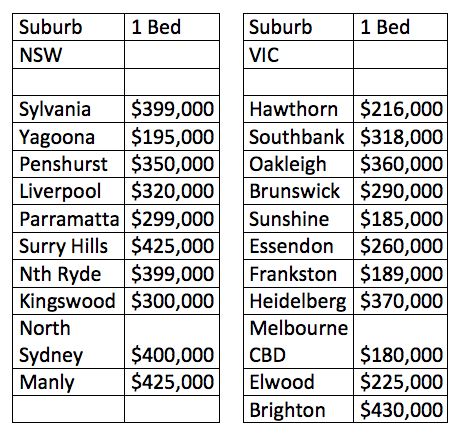

So as an exercise, I am going to show you where you can buy, and for how much. I am going to use various places throughout Sydney and Melbourne. Sorry for those in Brissy, Adelaide, ACT, Darwin, Hobart and Perth, but your prices are considerably cheaper and can be more easily achieved. Now I didn’t say ‘easy’, I said could be done ‘more easily’. And locations like the ACT offer share ownership for first homebuyers.

And as you can see by the suburbs chart above, I have fairly well covered all the major centres with suburbs right in the hub or the suburbs next door. These were all from live listings available as of early June 2016. I even added Melbourne CBD on Lonsdale St and Surry Hills as locations to show those who said they “HAD” to live within walking distance to work of the CBD.

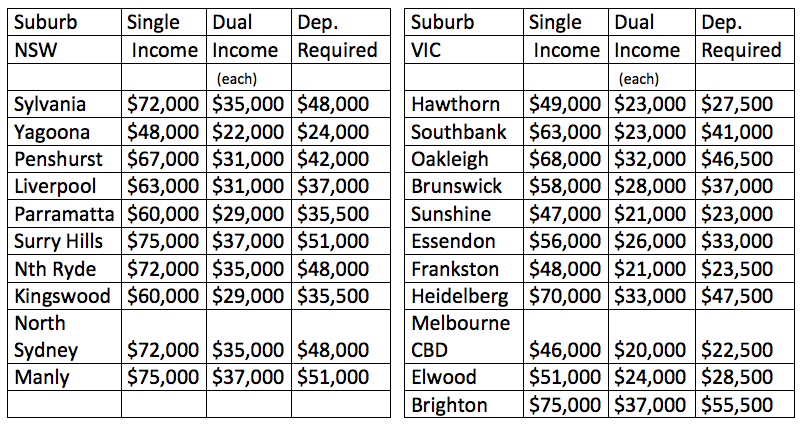

Now to back this up, I have added another chart below covering off how much income, single and a couple, require to service loans required for the above property prices. I have also added the deposit required to make this transaction happen.

Now I am sorry, but can anyone honestly say that buying your first home is not achievable?

Looking at the figures from both charts, I make the property prices to annual incomes between:

- 4 and 5.7 times for singles in Sydney

- 3.95 and 5.7 times for singles in Melbourne

- and for couple in both locations, the numbers are extremely close to the above numbers.

And hence my point, that the median income to median house price ratio is irrelevant in this argument!

I can already see the raft of abusive comments to follow this Blog. Things like, why should I have to live in a one-bedroom, dog box unit? Well that’s what most first homebuyers do, you spoilt brat! You buy what you can afford, where you can afford.

Remember; this isn’t going to be your home forever.

But what I see from all the comments, was that they were not willing to sacrifice where they are living to living further out from a CBD and having to travel to work. But you need to remember, the outter rings suburbs of Sydney and Melbourne are not new suburbs. They have been there for long before I purchased my first home. For example people have been traveling from Penrith to Sydney’s CBD for work almost 200 years!

So moving on, I would like to cover off on some comments relating to the so called ‘property crash’ they are expecting to happen. Now, I don’t have a crystal ball but I cannot see this happening, with one exception. I do see a reasonable price correction occurring but not until we see interest rates increase. But, then there will be complaints that they cannot afford it due to higher interest rates.

Even if Labor get in and abolish Negative Gearing, there will be small price decrease for around 1-2 years but you better hope that you are not renting and saving for a deposit if this happens as you will see significant rental increase on your next lease agreement. Again, making it hard to get into the market.

But using their logic, they want all property to crash, so it’s very affordable, so they can buy a home and then watch it increase in value and make money.

Isn’t that the exact thing you are currently complaining about?

I mentioned above about an exception to the property crash scenario. I do see a substantial correction occurring in the inner city high rise unit market due to huge oversupply issues. I believe it’s a ticking time bomb waiting to go off. There may be opportunities there for you shortly. If your happy to live in that “Dog Box”.

Now, you need to understand other world property markets to understand that our banking system and our monetary system works very differently to almost every other property market in the world. And because we have fairly good banking and lending regulations, a huge property crash is very unlikely.

The last comment from Part I that needs addressing was about that there are investors in the market currently simply to drive up prices. Really? So there are buyers out there with their sole purpose to buy properties for more than what they are worth and pay ridiculous prices so prices increase and push you out of the market. Sounds like a conspiracy theory to me.

So as I see this argument, the problem isn’t affordability (I’ve proven it’s very affordable), it’s the expectations of the Millenials wanting it all – NOW!!!

{kind=link}

{kind=link}